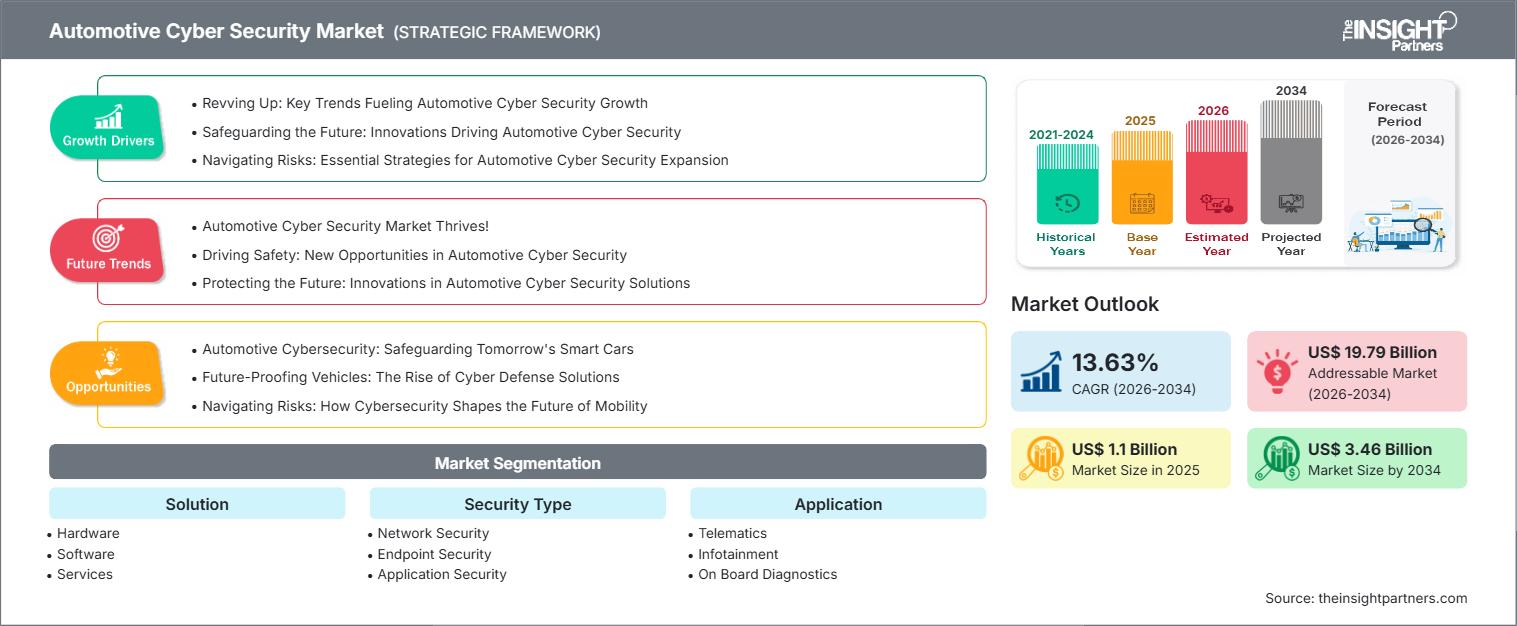

New York, June 19, 2026 (GLOBE NEWSWIRE) -- The Insight Partners published its latest market intelligence report on the Global Automotive Cybersecurity Market . The study finds the market, valued at US$ 7.23 billion in 2025, is projected to reach US$ 25.74 billion by 2034, registering a compound annual growth rate (CAGR) of 17.2% over the 2025 - 2034 forecast period. Research draws on primary interviews with C-suite executives, OEM engineers, procurement heads, and policy analysts across more than 15 countries, augmented by proprietary databases and third-party validation.

Market Overview

The automotive cybersecurity market encompasses a broad range of technologies, services, and solutions designed to protect vehicles, in-vehicle networks, electronic control units (ECUs), and connected mobility ecosystems from unauthorized access, cyberattacks, and digital threats. Key segments include in-vehicle network security (CAN, LIN, FlexRay, and automotive Ethernet), ECU and firmware security, telematics and infotainment security, over-the-air (OTA) update security, vehicle-to-everything (V2X) communication security, and cloud-based automotive backend protection. The market also includes security operations for connected vehicles, intrusion detection and prevention systems (IDPS), secure gateways, identity and access management for mobility systems, and automotive security lifecycle management aligned with embedded and software-defined vehicle architectures. Emerging areas include vehicle security orchestration and response platforms, AI-driven automotive threat detection, and hardware-based security modules integrated into next-generation vehicle platforms.

Demand is being driven by several structural tailwinds: rapid electrification, connectivity, and automation of vehicles, which is fundamentally increasing software complexity and expanding the automotive attack surface. The transition toward software-defined vehicles (SDVs), along with the widespread adoption of autonomous driving systems and connected mobility services, is accelerating the need for continuous and embedded cybersecurity across the vehicle lifecycle. In parallel, regulatory frameworks such as UNECE WP.29 and ISO/SAE 21434 are mandating formalized cybersecurity management systems for OEMs and suppliers, embedding security as a compliance requirement rather than a discretionary feature.

latest research on the Automotive Cybersecurity Market, covering market size forecasts, growth drivers, regulatory trends, and competitive insights. You may access the Sample document here: https://www.theinsightpartners.com/sample/TIPAT100001342

Key Market Findings

- Regional Leader: Europe is forecast to account for over 34.84% of global market share by 2031, led by the Germany and UK.

- North America: North America holds the second-largest share at over 25.44%, with the US has a dominating share.

- Dominant Segment: In-Vehicle Network Security retains the largest type segment share, driven by increasing focus on securing in-vehicle communication protocols such as CAN, LIN, FlexRay, and Ethernet against unauthorized access, spoofing, and malware injection across connected vehicle systems.

- Fastest-Growing Segment: Over-the-Air (OTA) Update Security registers the fastest CAGR, supported by rising adoption of software-defined vehicles, continuous feature updates, and increasing need to secure remote software deployment, patch management, and firmware integrity across vehicle fleets..

- Industry Vertical: Passenger Vehicles dominate the automotive cybersecurity market by vehicle type, driven by high production volumes, rapid integration of connected infotainment and telematics systems, and growing consumer demand for advanced connected car features and digital mobility services.

Primary Growth Driver: Rapid Vehicle Digitalization Coupled With Expanding Cyber-Physical Threat Landscape

The growth of the Automotive Cyber Security market can be primarily attributed to the rapid digital transformation of the automotive industry, marked by the rise of connected vehicles, electric vehicles (EVs), and software-defined vehicle (SDV) architectures. Modern vehicles are increasingly integrated with advanced electronics, telematics systems, infotainment platforms, and cloud-based mobility services, significantly expanding the in-vehicle and external attack surface. As vehicles become more connected to external networks through V2X communication, OTA updates, and mobile applications, exposure to cyber risks such as remote vehicle hacking, ECU manipulation, data theft, and safety-critical system disruption has increased substantially.

At the same time, the sophistication and frequency of automotive cyberattacks are rising, driven by organized cybercriminal groups, research-based exploit discovery, and potential state-sponsored threats targeting critical mobility infrastructure. This evolving threat environment is compelling OEMs, Tier-1 suppliers, and mobility service providers to invest heavily in advanced automotive cybersecurity solutions, including in-vehicle network security, secure gateways, intrusion detection systems, and cloud-based vehicle security platforms. The need to ensure passenger safety, protect vehicle data, and maintain functional integrity of safety-critical systems is becoming a core engineering and regulatory priority across the automotive value chain.

Connected Vehicle Cybersecurity Solutions: A High-Value End-Market

The connected vehicle cybersecurity segment forms a critical component of the broader automotive cybersecurity market, focusing on protecting vehicle electronics, communication networks, cloud platforms, and mobility ecosystems from cyber threats. This segment includes solutions such as in-vehicle network security systems, ECU and firmware protection, telematics security platforms, OTA update security mechanisms, V2X communication security, and automotive intrusion detection and prevention systems (IDPS). The primary objective is to ensure real-time threat detection, secure communication across vehicle systems, and continuous protection throughout the vehicle lifecycle—from manufacturing and deployment to post-sale software updates.

Modern automotive cybersecurity solutions are increasingly leveraging artificial intelligence and machine learning to identify anomalous vehicle behavior, detect zero-day vulnerabilities, and enable predictive threat mitigation across fleets. In addition, secure-by-design engineering principles and zero-trust architectures are being widely adopted to enforce strict authentication between ECUs, users, and external systems. Hardware-based security modules and cryptographic key management systems are also gaining strong traction as vehicles transition toward highly connected, autonomous, and software-driven mobility platforms requiring robust, scalable, and continuously updated security frameworks.

Get a customized report to align these insights with your strategic business objectives - https://www.theinsightpartners.com/customization/TIPAT100001342

Segment Analysis

In-Vehicle Network Security – Market-Leading Type Segment

The In-Vehicle Network Security segment forms the backbone of the automotive cybersecurity market, focusing on protecting in-vehicle communication networks such as CAN, LIN, FlexRay, and automotive Ethernet from unauthorized access, message spoofing, malware injection, and ECU-level intrusions. It includes technologies such as secure gateways, intrusion detection and prevention systems (IDPS), firewalls for automotive networks, and network segmentation solutions. The primary objective is to ensure secure and reliable communication between electronic control units (ECUs) while maintaining the safety, integrity, and functional stability of vehicle systems. In-vehicle network security solutions are increasingly evolving with the integration of artificial intelligence and machine learning, enabling real-time traffic monitoring, anomaly detection, and automated response to cyber-physical threats within the vehicle architecture.

Over-the-Air (OTA) Update Security – Growing at 18.5% CAGR

The Over-the-Air (OTA) Update Security segment is witnessing the fastest growth within the automotive cybersecurity market, driven by the rapid adoption of software-defined vehicles, continuous software upgrades, and the increasing need for remote diagnostics and feature enhancements. This segment focuses on securing the end-to-end OTA update lifecycle, including software delivery, authentication, encryption, and firmware integrity validation across vehicle fleets. The growing complexity of vehicle software ecosystems and the rising risk of malicious firmware injection and update tampering are accelerating demand for robust OTA security frameworks. OEMs and suppliers are increasingly deploying cryptographic security mechanisms, secure boot processes, and AI-driven anomaly detection to ensure safe, authenticated, and uninterrupted software updates across connected and autonomous vehicles.

Chat with us - https://tawk.to/chat/5d56720577aa790be32f2bec/default

Regional Analysis

Europe - Largest and Fastest-Growing Market

Europe dominates the global automotive cybersecurity market and is projected to account for a significant share of total market adoption by 2031, driven by strong automotive manufacturing ecosystems, stringent regulatory enforcement, and early implementation of vehicle cybersecurity standards. Germany remains the single largest national market, supported by the presence of leading OEMs, Tier-1 suppliers, and advanced engineering capabilities focused on software-defined and connected vehicles. France and the United Kingdom are also emerging as rapidly expanding markets, fueled by national cybersecurity strategies, increasing EV penetration, and rising investment in autonomous mobility and connected vehicle platforms.

North America - Sustained by Regulation and Digital Sovereignty Initiatives

North America holds the second-largest share of the global automotive cybersecurity market, driven by strong digital infrastructure, high penetration of connected vehicles, and the presence of leading automotive OEMs, autonomous driving companies, and cybersecurity solution providers. The United States remains the dominant market, supported by advanced R&D in vehicle software, strong adoption of telematics and infotainment systems, and increasing investment in vehicle-to-everything (V2X) communication security. Canada is also witnessing steady growth, fueled by rising adoption of smart mobility solutions, cloud-connected vehicle platforms, and increasing focus on transportation cybersecurity resilience.

Market Dynamics: Key Opportunities and Challenges

Rapid Vehicle Digitalization and Software-Defined Mobility: Key Growth Opportunity: The rapid transformation of the automotive industry toward connected, electric, and software-defined vehicles presents a significant growth opportunity for the automotive cybersecurity market. As vehicles increasingly integrate advanced electronics, telematics systems, infotainment platforms, and cloud-connected mobility services, the demand for robust cybersecurity solutions is rising sharply. This shift is driving strong investments in next-generation automotive security technologies such as in-vehicle network security, secure gateways, intrusion detection systems (IDPS), vehicle-to-everything (V2X) security, OTA update protection, and AI-driven threat intelligence platforms designed specifically for mobility ecosystems.

High System Complexity and Supply Chain Security Risks: Key Market Challenge: Despite strong growth prospects, the automotive cybersecurity market faces significant challenges related to high system complexity, legacy architecture integration, and fragmented supply chains. Modern vehicles consist of hundreds of interconnected electronic control units (ECUs) sourced from multiple suppliers, making end-to-end security implementation highly complex and costly. Additionally, securing the entire automotive software supply chain—including third-party software, firmware updates, and cloud-based mobility platforms—requires continuous monitoring, validation, and compliance with evolving standards such as UNECE WP.29 and ISO/SAE 21434. The shortage of specialized automotive cybersecurity talent further intensifies these challenges, limiting the ability of OEMs and suppliers to scale secure-by-design development across global vehicle platform.

Purchase the full report from The Insight Partners upto 40% Discounted Price - Automotive Cybersecurity Market

https://www.theinsightpartners.com/buy/TIPAT100001342/

Recent Industry Developments (2025 - 2026)

PIT Technologies announced the acquisition of Cymotive

In May 2026, PIT Technologies, a global leader in software solutions for the mobility ecosystem, today announced that it has entered into an agreement to acquire a majority stake in Cymotive, a leading automotive cybersecurity specialist headquartered in Israel. This acquisition shall strengthen KPIT’s strategic focus on building deep, future‑ready competencies required to deliver comprehensive software strategy and execution for mobility OEMs globally.

Shielding Innovation and Securing Mobility announced ThreatZ

In October 2025, VxLabs – Shielding Innovation and Securing Mobility announceed ThreatZ, a next-generation cybersecurity management and compliance platform that uses AI to help automotive security teams move with speed, efficiency, and consistency to protect connected, autonomous, and software-defined vehicles in a rapidly evolving threat landscape.

Leading Cybersecurity Companies

| Company | Profile |

| Bosch | Global automotive supplier offering integrated vehicle cybersecurity solutions, including secure gateways, ECU protection, and embedded security modules for connected and software-defined vehicles. |

| Continental AG | Leading automotive technology company providing cybersecurity architectures for in-vehicle networks, secure communication systems, and protection of connected mobility platforms. |

| HARMAN (Samsung) | Key player in connected car cybersecurity, specializing in secure infotainment systems, telematics security, and end-to-end vehicle software protection solutions. |

| BlackBerry QNX | Trusted provider of automotive-grade operating systems and cybersecurity solutions, enabling secure embedded systems and real-time protection for critical vehicle functions. |

| Aptiv | Global automotive technology company focused on software-defined vehicle architectures, offering cybersecurity solutions for vehicle networks, ADAS, and connected mobility ecosystems. |

| Airbiquity | Automotive software services provider specializing in OTA update security, connected vehicle data management, and secure telematics solutions for OEMs. |

| Karamba Security | Cybersecurity firm specializing in embedded vehicle security, ECU hardening, and real-time intrusion prevention systems for automotive networks. |

| Argus Cyber Security (Continental subsidiary) | Automotive cybersecurity leader focused on in-vehicle network protection, fleet security, and threat detection across connected and autonomous vehicles. |

| Upstream Security | Cloud-based automotive cybersecurity company providing fleet-level threat detection, data analytics, and security for connected vehicle ecosystems. |

| SafeRide Technologies | Specialized provider of AI-driven automotive cybersecurity solutions, focusing on anomaly detection, vehicle network protection, and autonomous vehicle security. |

About The Insight Partners

The Insight Partners is a globally recognized market research and management consulting firm specializing in technology, media, telecommunications, healthcare, and industrial sectors. Research methodology integrates primary data collection including executive interviews, OEM surveys, and channel partner analyses with proprietary secondary research databases and econometric modeling. Reports are used by Fortune 500 companies, private equity firms, government agencies, and institutional investors to inform strategic planning, M&A, and capital allocation decisions. The firm maintains research coverage across 50+ industries and 100+ countries.

Report Link: https://www.theinsightpartners.com/reports/cyber-security-market

Request for a free demo of The Insight Partners’ Automotive Cybersecurity Market & Intelligence Platform

Media Contact: The Insight Partners | sales@theinsightpartners.com | www.theinsightpartners.com

Also Available in : Korean | German | Japanese | French |Chinese | Italian | Spanish